What are 3 Main Types of Business Financial Statements?

The following are the main types of financial statements for a business:

- Balance Sheet: A snapshot of a business’s financial position (money the business owes to others and money owed to the business) at a specific point in time, including its assets, liabilities, and equity.

- Income Statement: A record of a business’s expenses and revenue over a specific period of time, such as a month or year, to determine its profitability.

- Cash Flow Statement: A record of a business’s incoming and outgoing cash flows over a specific period of time, showing how its operations, investing, and financing activities affect its cash position.

It’s important to note that the type of financial statements a business produces will depend on its size, industry, and jurisdiction. Larger companies may be required to produce more extensive financial statements, while smaller businesses may only need to produce a balance sheet and an income statement.

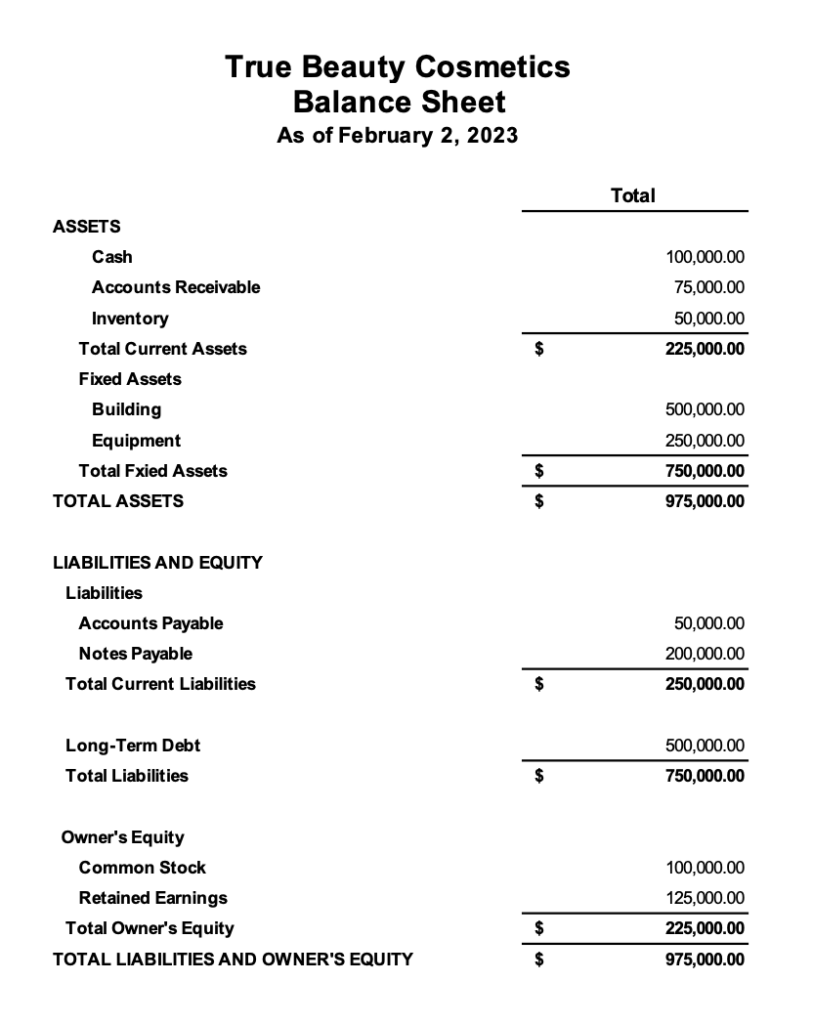

Balance Sheet

Assets

The assets section lists the resources a company owns or controls, with the intent of generating revenue. Assets are typically grouped into two categories: current assets that you expect will be converted into cash or used in the business within one year, and fixed assets, which are long-term resources such as property, plant, and equipment.

Liabilities

The liabilities section lists the debts and obligations a company owes to others. Liabilities are grouped into two categories as well: current liabilities that you expect will be paid within one year, and long-term liabilities, which are obligations that will be due beyond one year.

Owners' Equity

Owners’ equity represents the residual interest in the the company’s assets after deducting liabilities. Equity can be from a variety of sources, including common stock, retained earnings, and additional capital contributions.

The balance sheet must balance, meaning that assets must equal liabilities plus owners’ equity. This equation represents the accounting equation: Assets = Liabilities + Owners’ Equity.

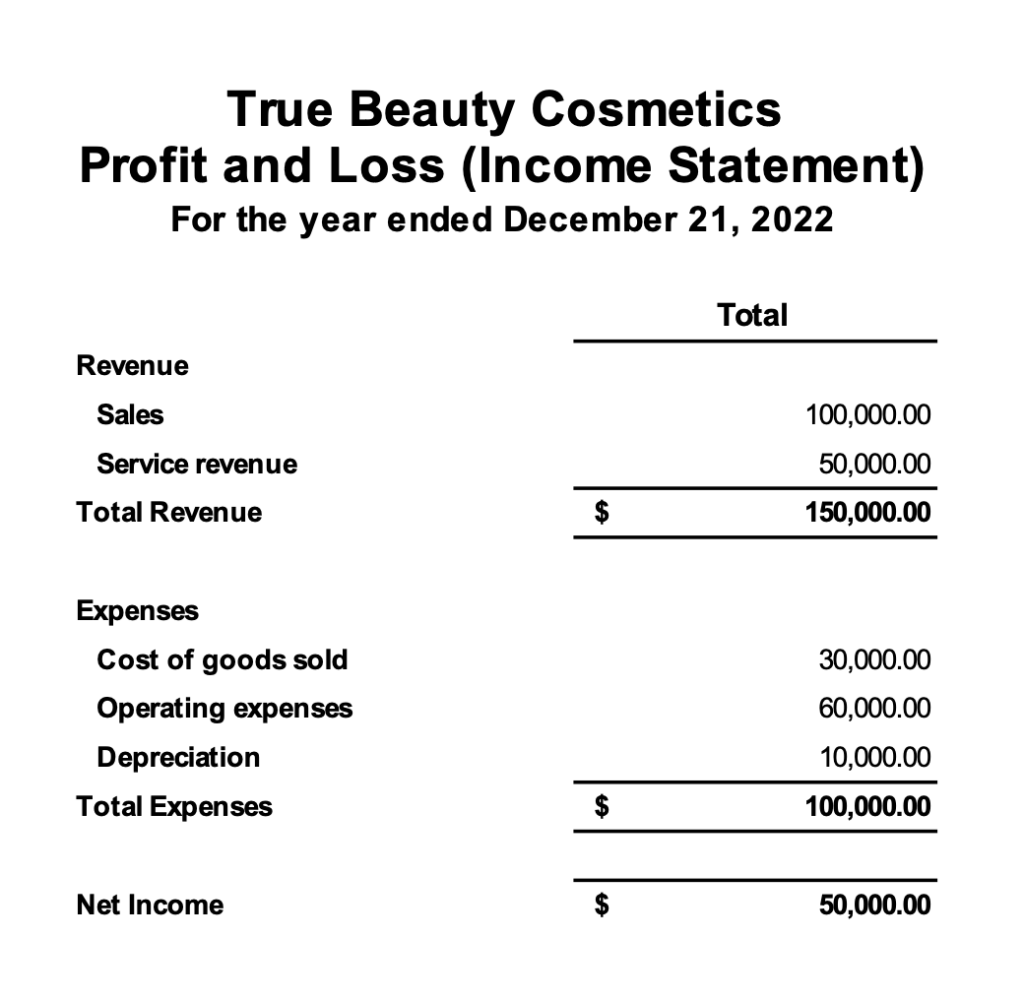

Income Statement (aka Profit and Loss Statement)

An income statement (aka profit and loss statement) reports a company’s revenues and expenses over a specified period of time, usually a year or a quarter. It shows the company’s ability to generate revenue, as well as its costs of doing business and the resulting profit or loss.

The income statement starts with revenue, which includes all the money the company has earned from its business activities. In this example, the company has two sources of revenue: sales and service revenue.

Next, the statement lists all expenses, which are the costs incurred to generate the revenue. In this example, the expenses are broken down into three categories: cost of goods sold, operating expenses, and depreciation. Cost of goods sold shows the cost of producing the goods sold to customers. Operating expenses are all other expenses involved in running the business, such as rent, utilities, and salaries. Depreciation is the decline in the value of a company’s assets over time.

Finally, the income statement shows the net income, which is calculated by subtracting total expenses from total revenue. In this example, the company had a net income of $50,000, which means it earned $50,000 more than it spent in the year.

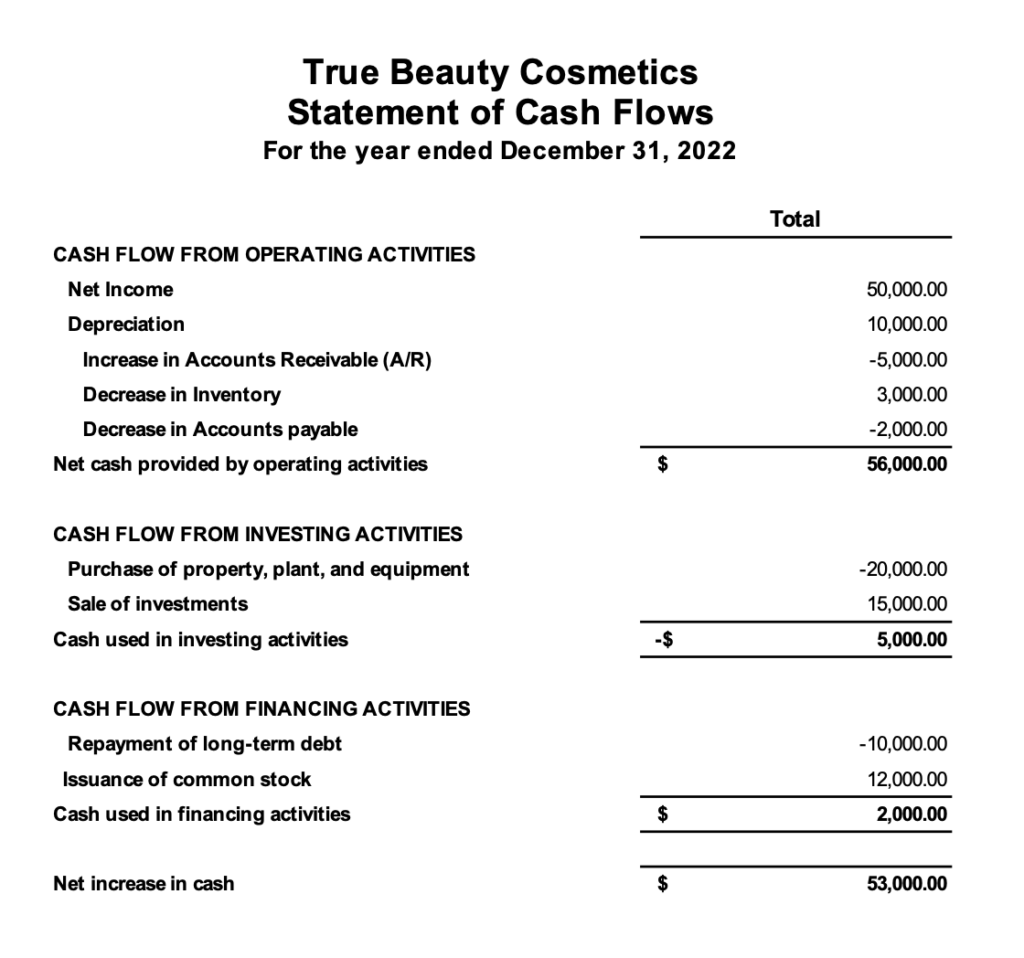

Cash Flow Statement

A cash flow statement is a business financial statement that provides information about the incoming and outgoing cash flow and cash equivalents for a company over a specified period of time, usually a year or a quarter. It helps to provide information about a company’s liquidity, or its ability to pay its bills, and to provide insight into a company’s financial health.

The cash flow statement starts with cash flow from operating activities, which is the cash generated from the company’s primary business activities, such as selling goods or services. In this example, the company had a net income of $50,000, which is adjusted for depreciation of $10,000 and changes in accounts receivable, inventory, and accounts payable.

Next, the statement shows cash flow from investing activities, which includes the cash used or generated from investments in long-term assets, such as property, plant, and equipment. In this example, the company used $20,000 to purchase property, plant and equipment, and generated $15,000 from the sale of investments.

Finally, the statement shows cash flow from financing activities, which includes the cash used or generated from financing sources such as debt or equity. In this example, the company repaid $10,000 of long-term debt and generated $12,000 from the issuance of common stock.

The last line of the statement shows the net increase in cash, which is the total decrease or increase in the company’s cash balance during the period. In this example, the company had a net increase in cash of $53,000.

These statements provide information about the sources and uses of income, expenses and cash during the period and help to provide insight into a company’s financial health.